Millions of Americans rely on Medicare for health coverage after age 65 or due to disability. But many soon realize that Original Medicare (Parts A and B) leaves them with out-of-pocket costs—like deductibles, copayments, and coinsurance—that can add up fast. That’s where Medicare Supplement Plans, also called Medigap, come in. These private insurance plans help cover the gaps in Medicare, giving you more predictable health care costs.

Choosing the right Medigap plan can feel overwhelming. There are several standardized options, different costs, and rules that change by state. This guide will break down the key differences, show side-by-side comparisons, and explain what really matters when choosing a plan.

If you want to protect your budget and make an informed decision, this article is for you.

What Are Medicare Supplement Plans?

Medicare Supplement Plans are insurance policies sold by private companies. They help pay some of the health care costs that Original Medicare doesn’t cover, such as:

- Deductibles (the amount you pay before Medicare pays)

- Coinsurance (your share of costs for services)

- Copayments (fixed amounts for services)

With Medigap, you still have Original Medicare. The supplement plan works as a “backup,” paying after Medicare pays its share.

Important: Medigap plans are not the same as Medicare Advantage plans. Medigap only works with Original Medicare, not with private Medicare Advantage plans.

The Different Types Of Medigap Plans

In most states, Medigap plans are standardized with letters: Plans A, B, C, D, F, G, K, L, M, and N. Each plan of the same letter offers the same basic benefits, no matter which insurance company sells it.

Not every plan is available in all states, and some (like Plan C and Plan F) are only available to people who became eligible for Medicare before 2020.

Here’s a quick overview of the most popular plans:

- Plan F: Covers almost all out-of-pocket costs. Only available if you qualified for Medicare before 2020.

- Plan G: Nearly identical to Plan F, but you pay the Part B deductible.

- Plan N: Lower premiums, but you pay small copays for doctor and emergency visits.

Plans K and L cover a percentage of costs, with out-of-pocket limits.

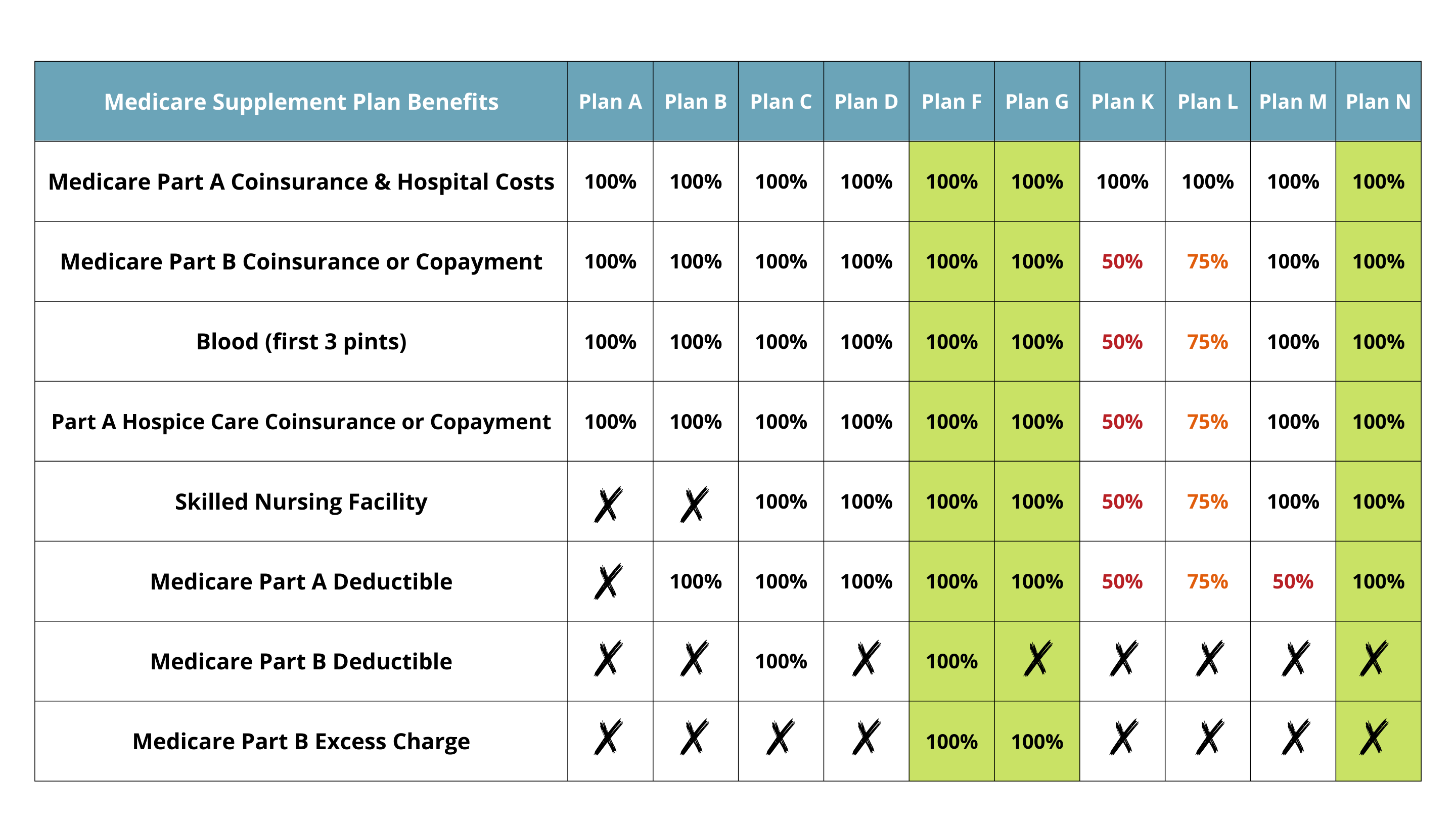

Medigap Plan Benefits Compared

To see how the main Medigap plans stack up, here’s a comparison of what each covers:

| Benefit | Plan F | Plan G | Plan N | Plan K | Plan L |

|---|---|---|---|---|---|

| Part A coinsurance & hospital costs | 100% | 100% | 100% | 100% | 100% |

| Part B coinsurance/copay | 100% | 100% | 100%* | 50% | 75% |

| Blood (first 3 pints) | 100% | 100% | 100% | 50% | 75% |

| Part A hospice care coinsurance/copay | 100% | 100% | 100% | 50% | 75% |

| Skilled nursing facility coinsurance | 100% | 100% | 100% | 50% | 75% |

| Part A deductible | 100% | 100% | 100% | 50% | 75% |

| Part B deductible | 100% | No | No | No | No |

| Part B excess charges | 100% | 100% | No | No | No |

| Foreign travel emergency (80%) | Yes | Yes | Yes | No | No |

| Out-of-pocket limit | None | None | None | $7,060 (2024) | $3,530 (2024) |

*Plan N requires copays: up to $20 for office visits and up to $50 for emergency room visits.

How Medigap Plans Differ

Coverage is not the only difference. Here are other key ways Medigap plans vary:

- Monthly premiums: Costs depend on plan, company, age, and location.

- Copays and deductibles: Some plans (like N) have small copays.

- Out-of-pocket limits: Only Plans K and L have maximum annual limits.

Let’s look at an example of premium ranges for a 65-year-old non-smoker in New York City:

| Plan | Monthly Premium Range |

|---|---|

| Plan F | $210 – $350 |

| Plan G | $180 – $320 |

| Plan N | $130 – $250 |

| Plan K | $60 – $110 |

| Plan L | $90 – $170 |

Premiums may be much lower or higher in other states. Companies can use different pricing methods—community-rated, issue-age-rated, or attained-age-rated—which affect how your premium changes over time.

Who Should Consider A Medigap Plan?

Medigap plans are best for people who:

- Want to keep Original Medicare and see any provider that accepts Medicare

- Prefer lower, more predictable out-of-pocket costs

- Travel often, including internationally (with Plans F, G, or N)

If you have frequent doctor visits or chronic conditions, a comprehensive plan like Plan G may be best. If you want lower monthly costs and can handle some copays, Plan N or Plan K could be a better fit.

What To Look For When Comparing Plans

Many people focus only on premium costs. But smart shoppers look beyond monthly price. Here’s what matters most:

- Coverage needs: Make a list of expected health care needs. Will you need skilled nursing, frequent doctor visits, or foreign travel coverage?

- Out-of-pocket costs: Add up not just premiums but also deductibles, copays, and coinsurance.

- Company reputation: Choose an insurer with strong financial ratings and good customer service.

- Rate increase history: Some companies raise rates more often than others.

- Guaranteed issue rights: If you apply during your Medigap Open Enrollment Period, you can’t be denied for health reasons.

A common mistake is choosing the cheapest plan without understanding limits or future rate hikes. Another is missing the open enrollment window, which can make it much harder or more expensive to get coverage.

Medigap Plan F Vs G Vs N: Which Should You Pick?

Let’s compare the three most popular plans for new enrollees.

Plan F

- Most complete coverage (all deductibles, coinsurance, and excess charges)

- Only available if you were eligible for Medicare before 2020

- Usually the highest premiums

Plan G

- Covers everything Plan F does except the Part B deductible ($240 in 2024)

- Available to all new enrollees

- Slightly lower premiums than Plan F

Plan N

- Lower premiums than F and G

- Covers most costs, but you pay up to $20 for doctor visits and up to $50 for emergency room visits

- Does not cover Part B excess charges (rare, but possible if your doctor charges more than Medicare allows)

Here’s a side-by-side summary:

| Feature | Plan F | Plan G | Plan N |

|---|---|---|---|

| Part B deductible | Covered | Not covered | Not covered |

| Part B excess charges | Covered | Covered | Not covered |

| Doctor visit copays | No | No | Yes ($20) |

| ER visit copays | No | No | Yes ($50) |

| Foreign travel coverage | Yes | Yes | Yes |

| Monthly premium (NYC) | $210–$350 | $180–$320 | $130–$250 |

Key insight: Plan G is now the most popular for new Medicare enrollees, because it offers nearly full coverage with only a small deductible.

Special Rules And State Differences

Some states have special Medigap rules:

- Massachusetts, Minnesota, and Wisconsin standardize plans differently (not by letter).

- Maine, Connecticut, and New York allow you to buy Medigap at any time, not just during open enrollment.

- In some states, insurers must offer Medigap to people under 65, but premiums may be much higher.

A non-obvious insight: In states with community rating, everyone pays the same premium regardless of age. In others, rates rise as you get older.

When And How To Enroll

The best time to buy a Medigap policy is during your Medigap Open Enrollment Period. This 6-month window starts the month you are 65 or older and enrolled in Part B. During this time:

- You can buy any plan sold in your state

- You cannot be denied or charged more due to health conditions

If you apply later, you could face higher costs or even be denied coverage due to pre-existing conditions.

Tip: Always compare several insurers—not just one—because premiums can vary widely for the same plan.

Common Mistakes To Avoid

- Missing your open enrollment window: After this, you may face medical underwriting.

- Choosing a plan based only on premium: The cheapest plan may come with higher out-of-pocket costs.

- Not checking company rate increase history: Premiums can rise quickly with some insurers.

- Assuming Medigap covers everything: It does not cover prescription drugs (you need a separate Part D plan).

- Buying Medigap when you have Medicare Advantage: You can’t have both at the same time.

Real-world Example

Mary, age 67, lives in Florida. She takes several prescription drugs and visits doctors often. She compares Plan G and Plan N. Plan G costs her $200/month, while Plan N is $140/month. She realizes her copays with Plan N would add up to $200 or more each year, and she’s worried about excess charges.

She chooses Plan G for peace of mind and avoids surprise bills. This shows why considering both premiums and out-of-pocket costs is so important.

Where To Get Reliable Information

The official Medicare site is the best starting point for up-to-date details and plan finders. Visit Medicare.gov to compare plans in your area, get pricing, and find local insurance companies.

Frequently Asked Questions

What Is The Difference Between Medigap And Medicare Advantage?

Medigap works with Original Medicare to help pay out-of-pocket costs. You keep the same Medicare doctors and hospitals. Medicare Advantage replaces Original Medicare with a private plan that may include drug coverage, dental, vision, and more, but often has a limited network.

Can I Change My Medigap Plan Later?

You can apply to change plans at any time, but after your open enrollment period, you may be denied or charged more due to health conditions. Some states have more flexible rules.

Does Medigap Cover Prescription Drugs?

No, Medigap plans do not include drug coverage. You must buy a separate Medicare Part D plan for prescriptions.

Are Medigap Premiums Tax-deductible?

In some cases, yes. If you itemize deductions, you may be able to deduct Medigap premiums as medical expenses. Check with a tax advisor for your situation.

What Happens If I Move To Another State?

Medigap plans are generally portable. You can keep your plan, but premium rates may change. In some cases, you may need to switch plans if you move to a state with different rules.

Choosing a Medicare Supplement Plan can protect you from high medical bills and give you peace of mind. Take time to compare options, look beyond just the monthly cost, and shop around for the best value. A little research now can save you thousands of dollars and a lot of stress later on.

Read More:

- Affordable Health Insurance Quotes: Save More on Quality Coverage

- Compare Family Health Insurance Plans: Find the Best Coverage

- Private Medical Insurance UK: Your Guide to Better Health Cover

- Best Private Health Insurance Plans: Top Choices for 2024

- Short Term Health Insurance Online: Compare Top Plans Instantly

- Medicare Dental and Vision Coverage: What You Need to Know

- Medicare Prescription Drug Plans: Save Big on Your Medications

- Best Medicare Advantage Plans: Top Picks for 2024 Coverage