Navigating Medicare Prescription Drug Plans can feel overwhelming, especially if you’re new to Medicare or English isn’t your first language. Yet, understanding how these plans work can help you save money, avoid surprises, and get the medicines you need. In this guide, we’ll break down everything you need to know about Medicare Part D—the prescription drug coverage—using clear language and practical tips. By the end, you’ll feel confident choosing the right plan for your needs.

What Are Medicare Prescription Drug Plans?

Medicare Prescription Drug Plans are insurance plans offered by private companies, approved by Medicare. These plans help pay for the cost of prescription drugs. This coverage is known as Medicare Part D. You can get Part D in two ways:

- Standalone Prescription Drug Plan (PDP): You add this to Original Medicare (Part A and Part B).

- Medicare Advantage Plan (MA-PD): Some Medicare Advantage plans (Part C) include drug coverage.

If you don’t enroll when you’re first eligible, you might pay a penalty later. So, it’s important to understand your options early.

How Medicare Part D Works

Each Part D plan has its own list of covered drugs, called a formulary. The formulary is organized into tiers. The lower the tier, the less you usually pay. Plans also set rules for how you get your drugs, like requiring prior authorization or limiting how much you can get at one time.

Key Features Of Part D Plans

- Monthly premiums: The price you pay each month for coverage.

- Annual deductible: The amount you pay out of pocket before the plan starts to pay.

- Copayments/coinsurance: Your share of the cost for each prescription.

- Pharmacy network: The list of pharmacies where you can fill prescriptions, often with lower prices at “preferred” locations.

Example Of Part D Costs

Here’s a typical breakdown for a 2024 Part D plan:

| Feature | Average Cost (2024) |

|---|---|

| Monthly Premium | $30–$50 |

| Annual Deductible | Up to $545 |

| Generic Drug Copay | $5–$15 |

| Preferred Pharmacy | Lower copays |

The costs vary by plan and location. Some plans offer $0 deductibles or lower premiums, but may cover fewer drugs.

Who Should Get A Prescription Drug Plan?

Most people with Original Medicare should consider Part D, even if they don’t take many medicines now. If you skip Part D when first eligible and later need it, Medicare charges a late enrollment penalty—an extra cost added to your premium for every month you delayed.

People with Medicare Advantage may already have drug coverage. Check your plan details, as not all Advantage plans include Part D.

If you have other drug coverage (such as from an employer or union), you may not need Part D. But make sure your coverage is “creditable”—meaning it’s at least as good as Medicare’s. Otherwise, you could face penalties.

How To Choose The Right Medicare Prescription Drug Plan

Choosing the best Part D plan depends on several factors. Here’s how to make a smart choice:

1. List Your Medications

Write down every prescription you take, including the dosage and frequency. Some plans cover certain drugs better than others.

2. Check The Plan’s Formulary

Each plan has its own formulary. Search for your medicines in their list. If your drug isn’t covered, you may pay the full price or need to switch medications.

3. Compare Costs

Look at:

- Premiums

- Deductibles

- Copays/coinsurance

- Out-of-pocket maximums

Use the Medicare Plan Finder tool to compare costs for your medicines across different plans.

4. Consider Pharmacy Options

Some plans have “preferred pharmacies” with lower prices. If you prefer mail-order, check if the plan supports it.

5. Review Extra Benefits

Some Part D plans offer extra services, like medication therapy management (MTM) or discounts on vaccines.

6. Check Ratings

Medicare rates plans from 1 to 5 stars. Higher ratings mean better service and fewer complaints.

7. Think About Travel Or Moving

If you travel often or plan to move, check if your plan covers pharmacies in other areas.

Comparing Popular Medicare Prescription Drug Plans

To help you see the differences, here’s a comparison of three popular Part D plans (2024 data):

| Plan Name | Monthly Premium | Deductible | Drug Coverage | Star Rating |

|---|---|---|---|---|

| SilverScript Choice | $30 | $0 | Wide (most generics & brands) | 4.5 |

| Humana Walmart Value | $35 | $545 | Good (main generics & brands) | 4 |

| Wellcare Classic | $40 | $545 | Moderate (many generics) | 3.5 |

As you can see, lower premiums may come with higher deductibles, and wider drug coverage usually costs more. Always match the plan to your personal medication needs.

Common Mistakes When Choosing A Plan

Many beginners miss these points:

- Ignoring the formulary: Not all plans cover every drug. Always check your medications.

- Choosing only by premium: Low premiums may mean higher costs elsewhere.

- Missing network pharmacies: Using a pharmacy outside the network can increase your costs.

- Not considering future needs: Even if you’re healthy now, medicines may change.

- Skipping annual reviews: Plans and formularies change yearly. Review your plan every fall.

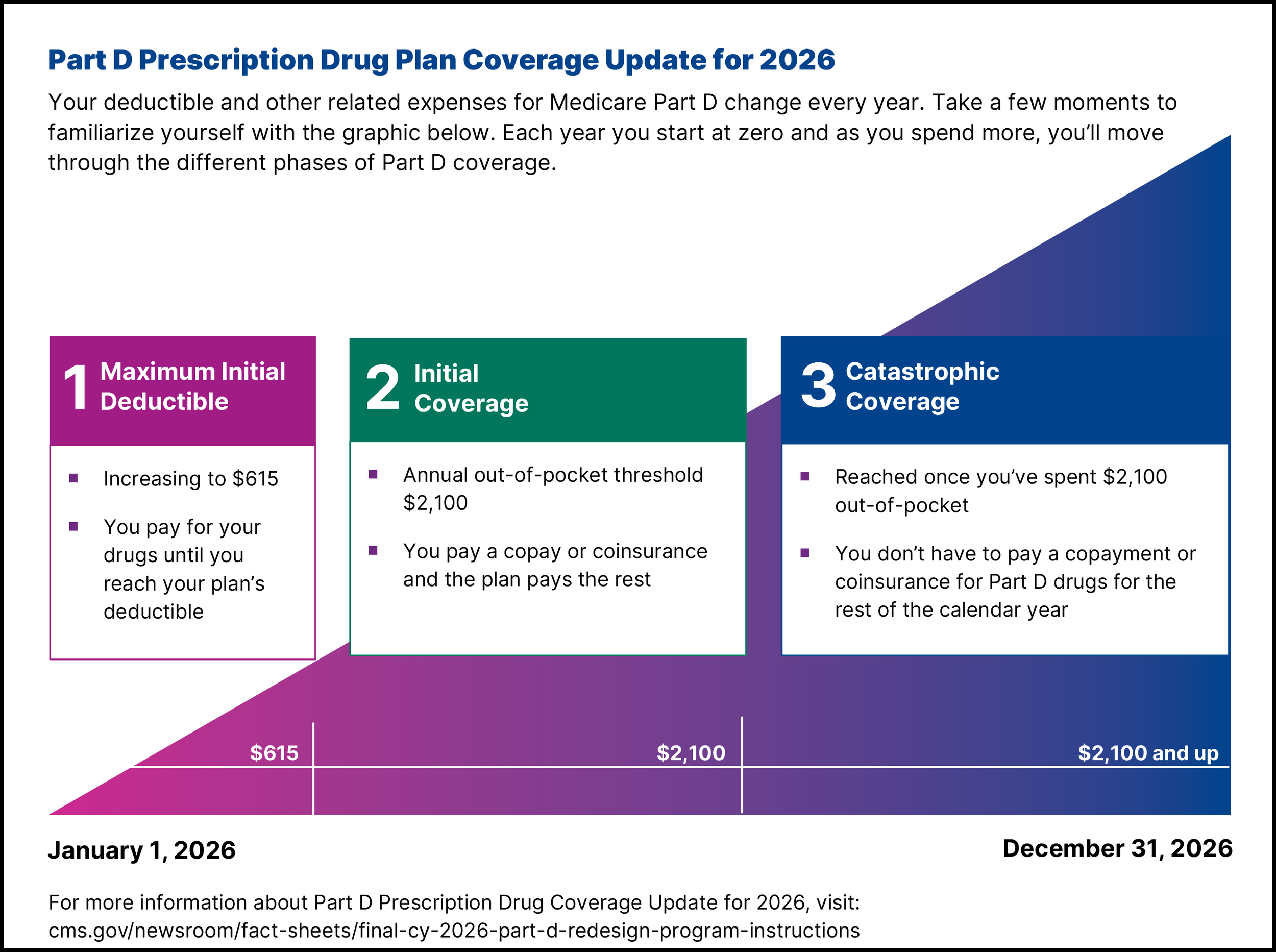

Understanding The Part D Coverage Stages

Medicare Part D has several coverage stages. Knowing these can help you plan your yearly expenses.

1. Deductible Stage

You pay 100% of drug costs until you reach the deductible (up to $545 in 2024).

2. Initial Coverage

After the deductible, you pay copays or coinsurance. The plan pays the rest.

3. Coverage Gap (“donut Hole”)

When your total drug costs reach $5,030 (2024), you enter the coverage gap. You pay 25% of the cost for most drugs.

4. Catastrophic Coverage

If you spend $8,000 out-of-pocket (2024), you pay much less for the rest of the year—usually just a small copay or nothing.

Here’s a summary:

| Stage | What You Pay | 2024 Threshold |

|---|---|---|

| Deductible | 100% | $545 |

| Initial Coverage | Copay/coinsurance | $5,030 |

| Coverage Gap | 25% | $8,000 |

| Catastrophic | Small copays | After $8,000 |

Extra Help: Reducing Costs For Low-income Individuals

Medicare offers Extra Help for people with limited income and resources. This program lowers Part D costs, including premiums, deductibles, and copays. In 2024, you may qualify if your income is below $22,000 (single) or $30,000 (married). Apply through Social Security or your local Medicaid office.

Some states also offer additional support, called State Pharmaceutical Assistance Programs (SPAPs). Check if your state provides extra help.

How To Enroll In A Medicare Prescription Drug Plan

You can enroll in Part D when you first become eligible for Medicare, during the Annual Enrollment Period (October 15–December 7), or during special enrollment periods if your situation changes.

Steps to enroll:

- Use the Medicare Plan Finder at medicare.gov.

- Compare plans by entering your prescriptions.

- Select a plan and enroll online, by phone, or by contacting the plan directly.

- Keep your plan information for pharmacy visits.

If you need help, local State Health Insurance Assistance Programs (SHIPs) offer free counseling.

Practical Tips For Managing Your Part D Coverage

- Keep a list of all your medicines—including over-the-counter drugs.

- Use preferred pharmacies for lower costs.

- Review your plan every year during open enrollment, even if you’re happy with it.

- If your drug is not covered, ask your doctor about alternatives or request a formulary exception.

- If you’re traveling, check if your plan covers pharmacies in your destination.

A common non-obvious insight: Many people don’t realize that drug prices can change during the year, even with the same plan. It’s wise to ask your pharmacist about price changes and look for generic alternatives.

Another tip: If you use expensive medicines, ask your doctor if you qualify for manufacturer discount programs. Sometimes, these can offer savings beyond your Part D plan.

Frequently Asked Questions

What Is The Penalty For Late Enrollment In Medicare Part D?

If you don’t sign up for Part D when first eligible and don’t have creditable drug coverage, Medicare adds a late enrollment penalty to your monthly premium. The penalty is 1% of the national average premium for every month you delayed enrollment.

Can I Change My Medicare Prescription Drug Plan After Enrolling?

Yes. You can change your plan each year during the Annual Enrollment Period (October 15–December 7). You may also qualify for a Special Enrollment Period if you move or lose other coverage.

What If My Medication Is Not Covered By My Plan?

If your medicine is not on your plan’s formulary, ask your doctor about alternatives. You can also request a formulary exception for medical necessity. Your plan will review your request.

How Do I Know If I Qualify For Extra Help?

You may qualify for Extra Help if your income and assets are below certain limits. Visit Social Security’s website or your local Medicaid office to apply. Extra Help can save you thousands of dollars each year.

Where Can I Get Unbiased Help Comparing Part D Plans?

Visit the official Medicare website (Medicare.gov) or contact your local State Health Insurance Assistance Program (SHIP) for free, unbiased counseling.

Choosing a Medicare Prescription Drug Plan isn’t just about finding the lowest price. It’s about making sure your medicines are covered, your pharmacy is convenient, and your plan fits your health needs. Take time to review your options, ask questions, and use available resources.

With the right plan, you’ll have peace of mind and the support you need for your health.

Read More:

- Affordable Health Insurance Quotes: Save More on Quality Coverage

- Compare Family Health Insurance Plans: Find the Best Coverage

- Private Medical Insurance UK: Your Guide to Better Health Cover

- Best Private Health Insurance Plans: Top Choices for 2024

- Short Term Health Insurance Online: Compare Top Plans Instantly

- Medicare Supplement Plans Comparison: Find the Best Coverage Now

- Medicare Dental and Vision Coverage: What You Need to Know

- Best Medicare Advantage Plans: Top Picks for 2024 Coverage