Private Medical Insurance Uk: A Complete Guide

Private medical insurance in the UK is becoming more popular. Many people want faster treatment, more comfort, and choices that the NHS (National Health Service) cannot always provide. Whether you are worried about long waiting lists, want specialist care, or simply prefer private hospitals, understanding private medical insurance is important before making a decision.

This article explains how private medical insurance works in the UK, who should consider it, what to look for in a policy, and common mistakes to avoid. You will also find real data, comparisons, and answers to the most frequent questions.

What Is Private Medical Insurance?

Private medical insurance is a policy you buy to cover healthcare costs in private hospitals or clinics. It pays for treatments, surgeries, and sometimes extras like dental and optical care. Unlike the NHS, which is free at the point of use, private insurance costs money.

It gives you access to private doctors, faster appointments, and sometimes better facilities.

Most UK residents still use the NHS for basic care, but private insurance can help with:

- Faster treatment for non-emergency issues

- Access to specialist doctors and consultants

- Private rooms during hospital stays

- More choice in hospitals and clinics

People often buy private insurance to avoid waiting for treatment, especially for planned surgeries or scans.

How Does Private Medical Insurance Work?

When you buy a policy, you pay a monthly premium. This is the price for your cover. If you need treatment, you can use your insurance to pay for private care. The policy will cover certain treatments, but not all. You usually need to get approval from your insurer before booking private care.

Some policies are comprehensive (covering most treatments), while others are basic (covering only major issues). Policies often have:

- Annual limits on spending

- Exclusions (things not covered)

- Options for extra cover (such as dental or mental health)

You can buy insurance for yourself, your family, or your employees (if you run a business).

Nhs Vs Private Medical Insurance

Most people in the UK rely on the NHS. So, why pay for private insurance? The main reasons are speed, comfort, and choice.

Here’s a comparison of some key differences:

| Feature | NHS | Private Insurance |

|---|---|---|

| Cost | Free (tax-funded) | Monthly premium |

| Waiting Times | Can be long | Usually shorter |

| Choice of Doctor | Limited | Wide choice |

| Hospital Room | Shared | Private |

| Specialist Access | Referral needed | Direct access |

Private insurance does not replace the NHS. You still use the NHS for emergencies, accidents, and some chronic conditions.

Who Should Consider Private Medical Insurance?

Private medical insurance is not for everyone. It’s most useful for people who:

- Want to avoid NHS waiting lists

- Need planned or elective surgery

- Value privacy and comfort during hospital stays

- Have family history of certain illnesses

- Travel often and want extra health security

Some employers offer private medical insurance as a benefit. If you are self-employed or run a small business, you may consider covering yourself or your team.

What Does Private Medical Insurance Cover?

Coverage depends on the policy. Most standard policies include:

- Inpatient treatment (hospital stays and surgeries)

- Outpatient treatment (consultations, scans, tests)

- Cancer care (some policies offer full cover)

- Specialist consultations

Some policies offer extras, such as:

- Dental care

- Optical (eye) care

- Physiotherapy

- Mental health support

But not everything is covered. Common exclusions are:

- Pre-existing conditions

- Chronic illnesses (like diabetes)

- Emergency treatment (still NHS)

- Pregnancy and childbirth

Always read the policy documents carefully.

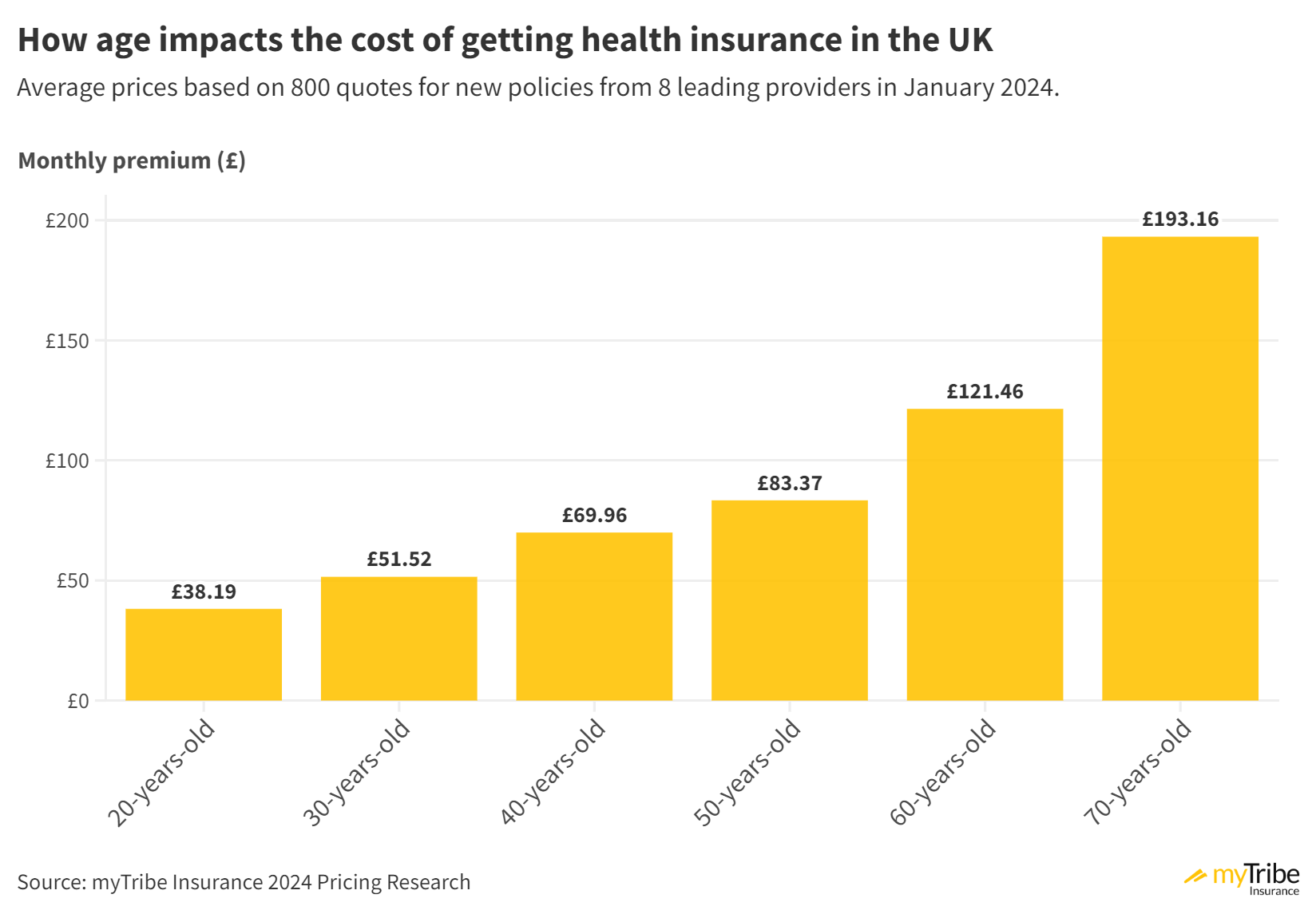

How Much Does Private Medical Insurance Cost?

Prices vary widely. Your age, health, location, and chosen cover all affect the cost. In 2023, average monthly premiums for a single adult ranged from £40 to £100. Family cover is usually higher.

Here’s a sample breakdown:

| Type of Cover | Average Monthly Premium | Typical Age Range |

|---|---|---|

| Basic | £40–£60 | 25–40 |

| Comprehensive | £70–£120 | 40–60 |

| Family | £120–£250 | All ages |

You can reduce costs by:

- Choosing higher excess (the amount you pay before insurance covers)

- Limiting hospital choices

- Excluding outpatient care

But be careful. Cheap policies may not cover what you need.

Choosing The Right Policy

Picking the best policy is not simple. Here are the key factors to consider:

- Coverage: What does the policy include? Inpatient, outpatient, cancer care, extras?

- Excess: How much will you pay out of pocket?

- Hospital List: Which hospitals and clinics can you use?

- Waiting Periods: Is there a waiting period for pre-existing conditions?

- Extras: Do you need dental, optical, or mental health cover?

- Premiums: Can you afford the monthly payments?

- Customer Service: Is the insurer easy to contact and helpful?

Many beginners forget to check hospital lists. Not all policies cover every hospital. Another common mistake is ignoring excess. A high excess can make insurance cheap, but you pay more when you claim.

Common Mistakes To Avoid

People often rush into buying private medical insurance. Here are mistakes to avoid:

- Not reading the policy exclusions

- Ignoring excess costs

- Assuming all private hospitals are covered

- Forgetting to declare pre-existing conditions

- Choosing the cheapest option without checking cover

For example, some policies exclude cancer treatment, while others offer full cover. Always compare policies carefully.

Real-life Examples

Let’s look at two examples:

Case 1: Emma, 38, bought a basic policy for £45/month. She needed a knee operation. Her insurer covered the surgery, but only at certain hospitals. She paid £250 excess.

Case 2: John, 50, chose a comprehensive policy for £110/month. When he needed cancer treatment, his insurance paid for specialist care, private room, and chemotherapy with no extra cost.

These cases show why details matter. Cheaper policies may limit choices, while full cover is more expensive but gives peace of mind.

Data On Private Medical Insurance In The Uk

Private health insurance is a growing market. In 2022, over 4 million people in the UK had private medical insurance. That’s about 6% of the population. Most people are covered through their employer, but individual policies are rising.

According to the Association of British Insurers, claims paid in 2021 totaled £1.7 billion. The most common claims were for diagnostics, surgeries, and cancer care.

Comparing Top Uk Providers

Here’s a quick comparison of popular UK insurers:

| Provider | Strengths | Weaknesses |

|---|---|---|

| Bupa | Wide hospital network, strong cancer cover | Premiums can be high |

| AXA Health | Flexible policies, good outpatient cover | Limited extras on basic plans |

| Vitality | Rewards for healthy lifestyle, mental health support | Some claims need approval |

| Aviva | Affordable family cover, digital GP service | Restricted hospital list on cheaper plans |

Always compare at least three providers before buying.

Is Private Medical Insurance Worth It?

This depends on your needs and budget. If you rarely need medical care and are happy with the NHS, insurance may not be needed. But if you want fast access, specialist care, or extra comfort, insurance can be valuable.

One insight many beginners miss: Private insurance does not cover emergencies. You still need the NHS for accidents, heart attacks, or serious illnesses. Another important point is policy renewal. If you claim often, premiums can rise.

Practical Tips For Buying Private Medical Insurance

If you decide to buy, follow these practical steps:

- Check your NHS options first. Sometimes, local NHS services are fast and effective.

- Use online comparison tools to see different policies and prices.

- Ask for a hospital list and read the exclusions.

- Choose an excess that fits your budget.

- Consider extras only if you really need them.

- Review your policy every year. Your needs may change.

Many people overlook the option to mix NHS and private care. For example, use the NHS for emergencies and private insurance for planned surgeries or specialist consultations.

Private Medical Insurance And Pre-existing Conditions

Most insurers do not cover pre-existing conditions. If you have a medical issue before buying, you may not get cover for that illness. Some insurers offer limited cover after a waiting period (usually two years), but this varies.

If you have chronic health problems, check policy details carefully. Some policies offer moratorium underwriting, which may cover new issues but not old ones.

Family And Group Policies

Buying for a family or group can be cost-effective. Family policies cover children, partners, and sometimes parents. Group policies for businesses usually offer discounts and extra benefits.

But check who is covered. Some policies limit age or exclude certain family members. Always ask about group discounts and extras.

Frequently Asked Questions

What Is The Difference Between Private Medical Insurance And Nhs?

The NHS is free and provides care to everyone. Private medical insurance is paid for and gives access to private hospitals, faster treatment, and more comfort. But emergencies and chronic illnesses are still handled by the NHS.

Does Private Medical Insurance Cover Emergencies?

No. Private insurance does not cover accidents or emergency treatment. You must use the NHS for urgent care like heart attacks, strokes, or injuries.

Can I Use Both Nhs And Private Insurance?

Yes. Many people use the NHS for emergencies and private insurance for planned treatments or specialist care. You can mix both for best results.

How Do I Claim With Private Medical Insurance?

Contact your insurer before booking treatment. They will approve your claim, tell you which hospitals you can use, and explain what is covered. Always follow their process for faster payment.

Will My Premiums Increase If I Claim Often?

Yes. Most insurers raise premiums if you claim regularly. Review your policy each year and ask about renewal terms.

Private medical insurance in the UK offers real benefits, but it is not a simple decision. Weigh your needs, compare policies, and ask questions. With careful planning, you can find the right cover for your health and peace of mind.

Read More:

- Affordable Health Insurance Quotes: Save More on Quality Coverage

- Compare Family Health Insurance Plans: Find the Best Coverage

- Best Private Health Insurance Plans: Top Choices for 2024

- Short Term Health Insurance Online: Compare Top Plans Instantly

- Medicare Supplement Plans Comparison: Find the Best Coverage Now

- Medicare Dental and Vision Coverage: What You Need to Know

- Medicare Prescription Drug Plans: Save Big on Your Medications

- Best Medicare Advantage Plans: Top Picks for 2024 Coverage